With so much at stake, it's little wonder so many Americans struggle with the decision of when to claim their Social Security.

Choosing when to claim Social Security can be one of the most important decisions you make about your retirement. Since the amount of money you receive in Social Security over a lifetime is determined by life expectancy, claiming earlier than your full retirement age results in smaller checks for a longer period of time, and claiming later than your full retirement age results in bigger checks for a shorter period of time.

Because of this, a lot of debate over when to claim centers on a person's health. However, the time value of money should also be considered, especially if other sources of retirement income allow you to invest your Social Security income.

Did you know?

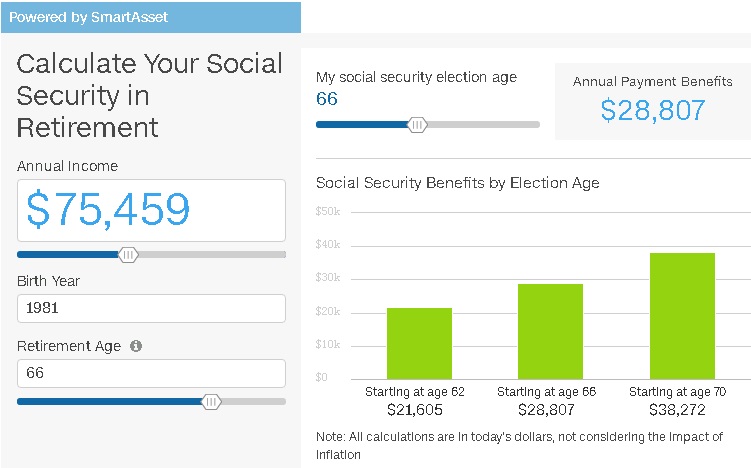

Full retirement age, or the age at which you can receive 100% of your Social Security benefit, is currently 66, but full retirement age increases steadily to 67, depending on your year of birth.

A person with a full retirement age of 66 who claims Social Security at 62 receives 75% of the amount they'd receive at his or her full retirement age. Conversely, a person with a full retirement age of 66 who waits until age 70 to begin receiving Social Security receives 32% more than he or she'd receive at full retirement age.

For many people, the guaranteed increase in Social Security income that comes from waiting to claim is appealing; however, the benefit of larger checks should be considered in the context of having forgone years of smaller checks. Calculating the breakeven point, or the point at which the total amount you collect from Social Security by waiting eclipses the amount you would have received by claiming early, may make those bigger checks less attractive.

Breaking even on waiting to claim Social Security

Social Security rewards people who wait to claim with an 8% annual increase for every year beyond full retirement age they delay receiving benefits.

That's a handsome return; however, despite that increase, you won't break even on your decision to wait until you reach about 80 years old.

For example, if you are slated to receive $1,000 per month at full retirement age, you can receive $750 per month if you claim at age 62 or $1,320 per month if you claim at age 70.

If you claim at age 62, you would collect a total of $81,000 in Social Security benefits at age 70, $135,000 in benefits at age 75, and $171,000 in benefits at age 80.

Alternatively, if you claim at 70, you would pocket $95,040 in benefits at age 75 and $174,240 in benefits at age 80. It's not until you reach 80 that the amount that you have collected in Social Security surpasses the amount you would've collected by claiming at age 62.

Calculating the impact of time

The problem with the straight-line breakeven analysis provided above is that it doesn't take into account the potential to earn a return on the money that is received if you claim Social Security when you're younger.

Although the number of retirees with pensions or other sources of retirement income in addition to Social Security is shrinking, many Americans still generate retirement income outside of Social Security, and for them, claiming Social Security later in life could be a mistake.

For example, if you receive a pension that can cover your retirement expenses and you claim early, you could invest your $750 per month in Social Security income rather than spend it. If you did that and earned a hypothetical 6% annually, then you could end up with a portfolio valued at $422,966 at age 85 and $616,758 at age 90. Waiting and investing your $1,320 per month in the same investment produces a nest egg worth only $368,693 at age 85 and $582,686 at age 90.

Consider carefully

There are a lot of personal reasons why you might want to claim Social Security early or wait to claim it, but if you have the financial flexibility to take advantage of the time value of money, waiting may not make as much sense as claiming early. Having said that, carefully consider all your Social Security options, including various claiming strategies, before you make your final decision. After all, if you claim early and change your mind, you only have one year to withdraw your claim.

The $15,834 Social Security bonus you could be missing

If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income.

For example: one easy trick could pay you as much as $15,834 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after.

- Publish my comments...

- 0 Comments